Quick CV Dropoff

Looking for your next opportunity? Upload your CV and one of our specialist consultants will review your details and get in touch if we have a suitable role that matches your skills and experience.

Our latest report below analyses data from the non-profit sector for:

The data below was obtained between January - March 2026 from non-profit specialist job boards agencies, and national labour market statistics.

Key non-profit trends this quarter:

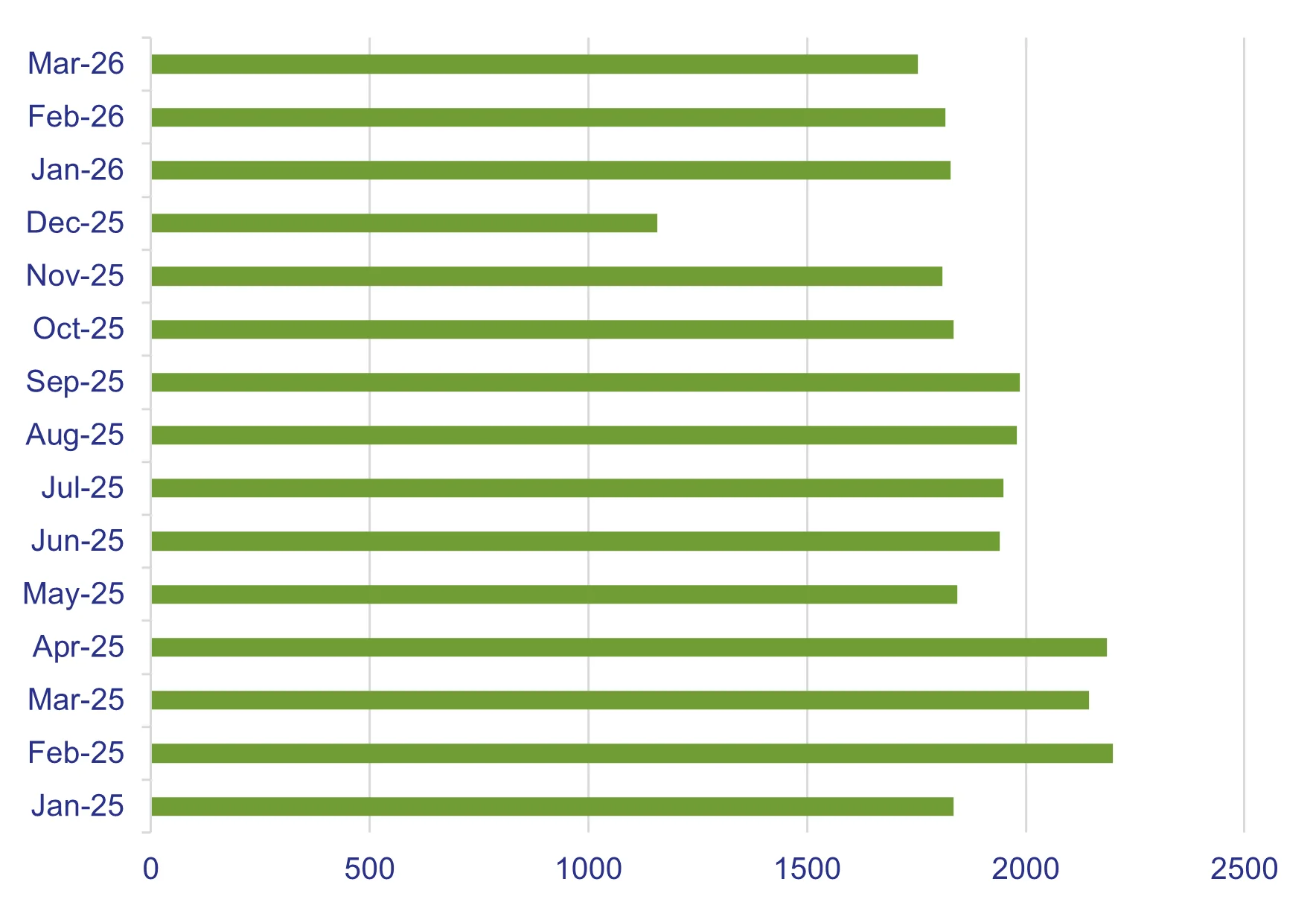

Vacancy levels softened slightly in Q1, reflecting a labour market that remains cautious following a prolonged period of contraction. Early ONS estimates show total vacancies falling by 6,000 roles (- 0.8%) to 721,000 between December 2025 and February 2026, though levels have remained broadly flat since spring 2025 and the change sits within the ONS confidence interval.

Within the non-profit sector specifically, vacancy volumes increased quarter‑on‑quarter compared to Q4, reflecting the usual seasonal rebound following the end-of-year slowdown. However, this uplift masks a wider trend: advertised roles remain materially lower than the same period last year, indicating that hiring demand has not yet returned to pre‑2025 levels.

While vacancy numbers continue to sit below last year’s figures, the absence of further quarter‑on‑quarter decline suggests a market that has stabilised rather than continued to weaken. This is consistent with wider labour market indicators, which point to restrained but sustained recruitment activity rather than renewed expansion.

This relative stability is particularly notable when viewed alongside emerging shifts in candidate behaviour. Increased application volumes and rising availability across temporary and fixed-term markets suggest a gradual rebalancing, with labour supply beginning to catch up with subdued hiring demand.

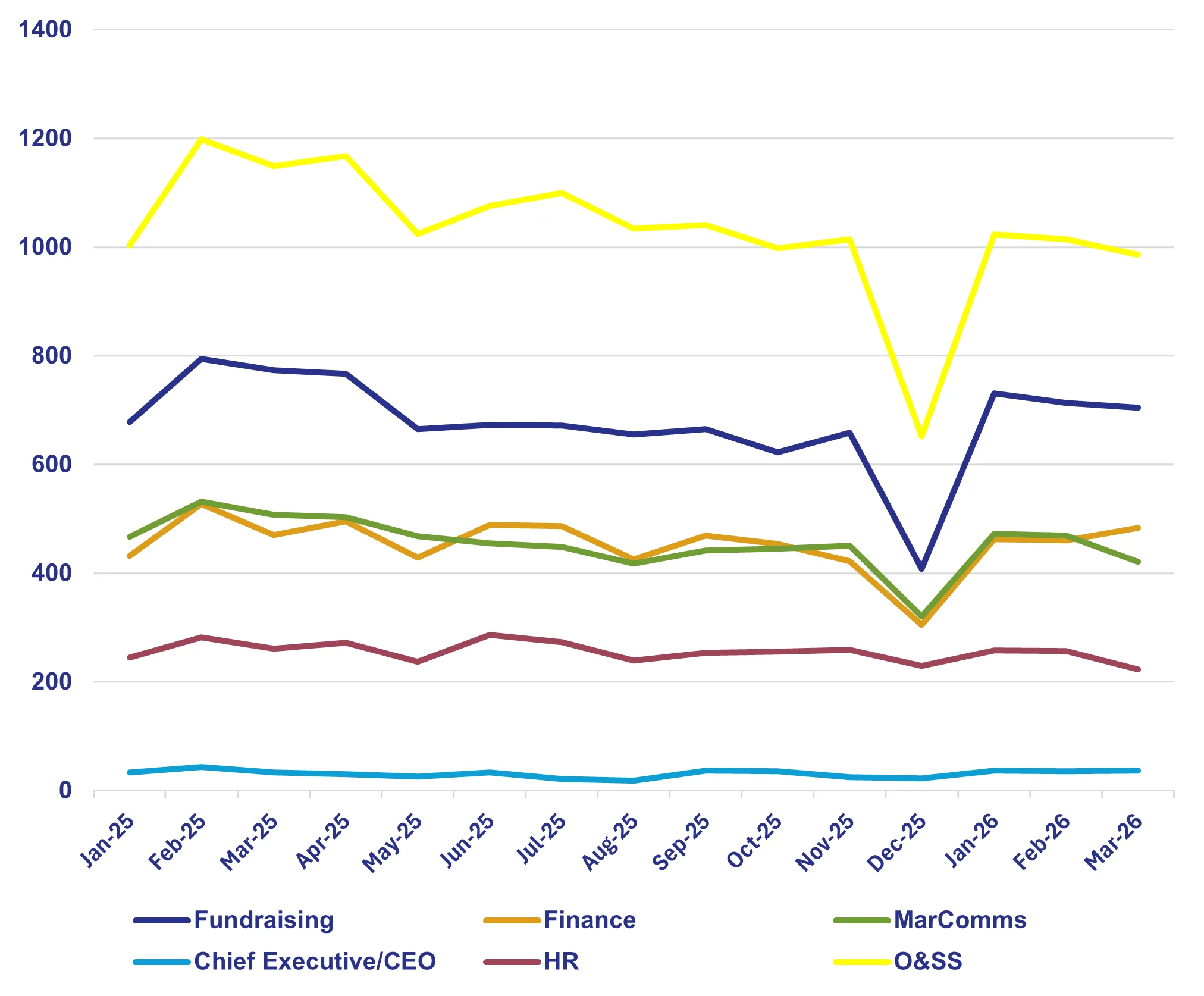

*O&SS - This includes roles in administration, PA & executive support, operations, legacy support, membership, programmes, projects, research & policy, data, supporter care.

Advertised roles increased across most job functions in Q1 following a seasonal Q4 dip, with the exception of HR, which saw a marginal further decline. Despite this quarterly uplift, demand remains lower year‑on‑year across all disciplines.

Finance vacancies saw a late Q1 uplift, potentially linked to year‑end reporting and planning activity, in contrast to the same period last year. Whether this represents a short‑term timing effect or an emerging trend will be important to monitor.

Data tracked here is for live vacancies within the non-profit sector advertised as permanent, temporary and fixed-term contract.

The mix of permanent, temporary and contract roles remained broadly consistent in Q1, with only minor quarter‑on‑quarter movement.

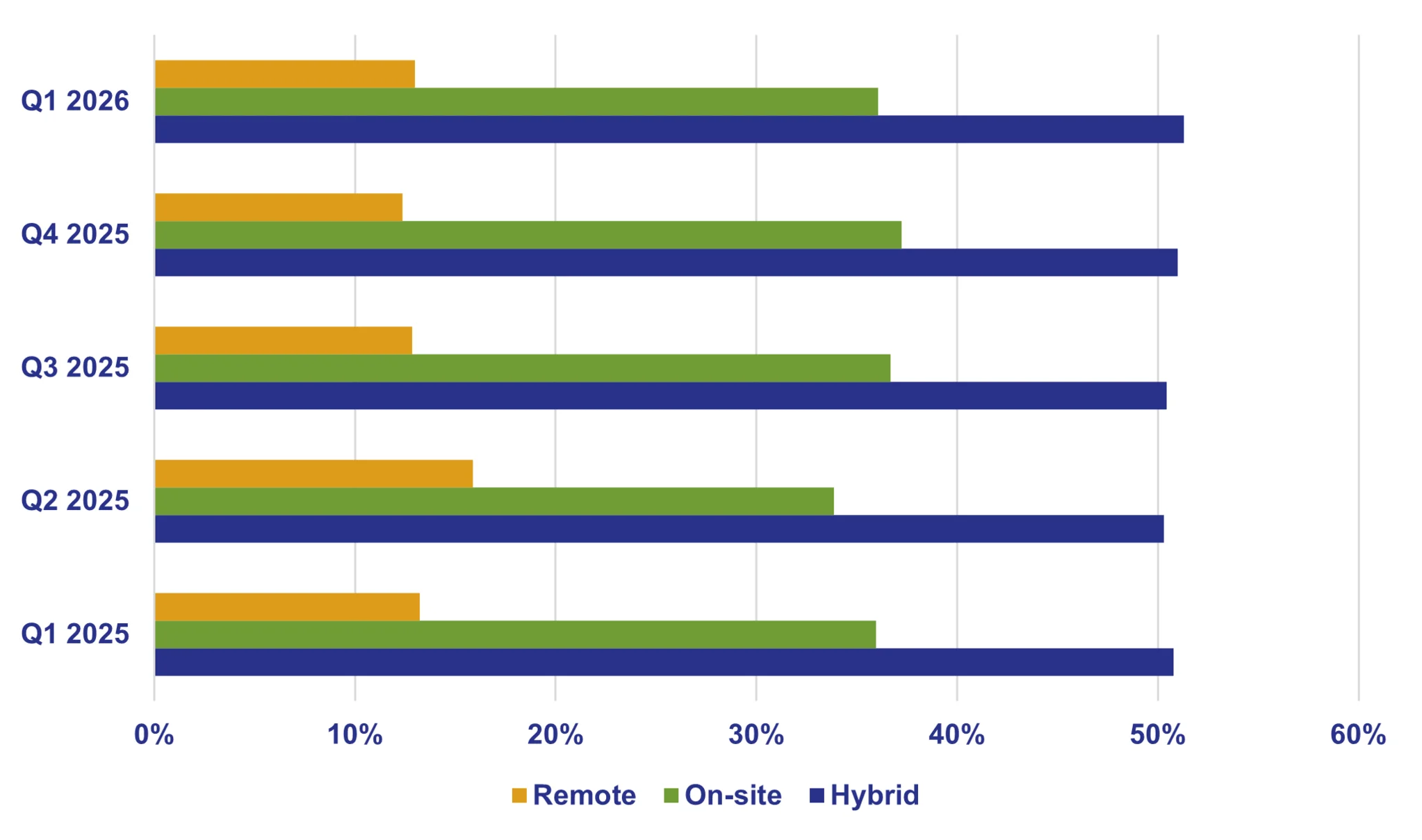

Hybrid working remained the dominant model in Q1, continuing to account for just over half of all advertised roles and showing little change quarter‑on‑quarter. This reinforces hybrid as the established and preferred working model across the non‑profit sector.

While previous quarters had hinted at a gradual shift towards more on‑site roles, Q1 data shows a modest reverse of this pattern, with a slight decrease in on‑site roles and a small increase in fully remote vacancies. Taken together, this suggests continued fine‑tuning of location expectations by employers, rather than any fundamental change to flexible working practices.

Whilst 2025 saw entry level role numbers remain consistent at an already low average of 10% of all live vacancies, Q1 has seen this decrease even further to its lowest level since our Non-Profit Recruitment Insights Reports began. On average, entry level roles are now sitting at 9% of all live vacancies, however this has been steadily decreasing since January with March levels showing only 8%. We have also not seen overall average vacancy numbers for entry level roles increase this quarter staying at the same levels as Q4 where we would expect a seasonal dip.

This continued contraction raises concerns around future talent pipelines, particularly at a time when many organisations are already grappling with skills shortages and succession planning challenges. Sustained under‑investment at entry level risks storing up longer‑term recruitment pressures across the sector.

Applications to live roles increased by 24% quarter‑on‑quarter in Q1, reaching their highest level since Q2 2025, despite remaining significantly lower than the same period last year (down 58% year‑on‑year).

While the start of the year is typically associated with an increase in candidate activity, the rise seen in Q1 follows several quarters of increasingly selective application behaviour. This suggests a more pragmatic shift in mindset among jobseekers, with candidates broadening their search activity in response to continued market uncertainty and a constrained permanent hiring landscape, rather than renewed confidence in job opportunities.

Candidate availability continued to diverge by job type in Q1. Permanent candidate availability declined both quarter‑on‑quarter (down 14%) and year‑on‑year (down 19%), while availability in the temporary and fixed‑term markets increased. Temporary availability rose by 10% quarter‑on‑quarter, marking the third consecutive quarterly increase, while fixed‑term availability edged up marginally both quarter‑on‑quarter and year‑on‑year.

This shift suggests candidates may be prioritising flexibility and security in the short term, with many showing greater openness to temporary and fixed‑term roles in response to continued caution in the permanent hiring market. For employers, this may present opportunities to access wider talent pools on a non‑permanent basis, while also highlighting ongoing challenges in attracting candidates into long‑term roles amid sustained market uncertainty.

Q1 data continues to reflect a market that has settled into a period of steadier activity rather than meaningful growth. While demand remains controlled, rising candidate availability, particularly across temporary and fixed‑term roles, has started to create more workable hiring conditions for organisations able to adapt their approach as 2026 unfolds.

Recruitment activity through Q1 has remained active but measured, with decision‑making increasingly influenced by short‑term risk management and delivery priorities. Organisations that remain clear on their objectives, open to flexible resourcing models and proactive in engaging candidates are best positioned to navigate the current environment and build capability across the remainder of 2026.